How is Credit Calculated?

Credit score is compiled of a few factors that are listed in your credit report. Your credit information is compared to other borrowers like you to create your credit score.

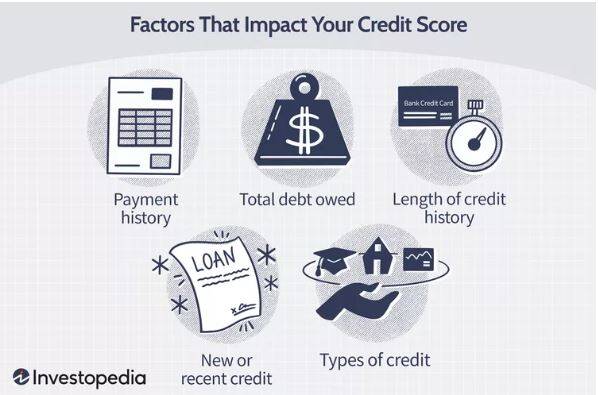

What Goes Into a Credit Score?

Payment History: 35-40%

Whether an individual pays their credit accounts on time. Credit reports show the payment history for each line of credit that you have and reports any late or missing payments. Your payment history is the most important aspect of your credit score, because it shows how you’ve managed your finances.

Credit Utilization: 20-30%

The amount of money an individual owes. Having a lot of debt does not necessarily give you a low credit score. Instead, credit scores typically consider the percent of your total available credit that you are using.

Length of Credit History: 15-21%

How long a person has had credit. Generally, the longer you've had credit, the higher your score will be. Your credit score considers how long the oldest account has been open, the age of the newest account, and the overall average. Your credit history is also very important, as it demonstrates how long you've been managing your accounts, when your last payments were made, and any recent charges.

Credit Mix: 10-11%

Your credit mix refers to the different types of credit you have, such as credit cards and mortgages. In general, you should have a mix of retail accounts, credit cards, loans, and mortgages.

New Credit: 8-10%

Recently opened accounts. If a borrower has opened a bunch of new accounts in a short period of time, that indicates risk and lowers their score.

Some lending institutions also consider available assets and the number of liabilities you have when they determine the probability of default.

What is Not Included in a Credit Score?

- Age

- Ethnicity

- Religion

- Marital status

- Employer

- Salary

- Occupation

- Other Personal Demographics

What is FICO?

The credit score model created by the Fair Isaac Corp., now known as FICO, is the most commonly used credit scoring method. The main alternative to the FICO Score is VantageScore. Like FICO Scores, the VantageScore rates an individual's creditworthiness on a scale of 300 to 850, based on factors like payment history, credit mix, and credit utilization. However, the VantageScore attaches different weights to those factors, so your VantageScore may be slightly different from your FICO Score.

Why is Your Credit Score Different Depending on Where You Look?

Your credit score may be different depending on who gives it to you because the scoring models used may be different. For example, the model used by your bank or lender may be different than the one used when you get your score from TransUnion. The different scoring models typically look at the same factors but put different weights on the different factors. For example, in some agencies, the amount owed may have a larger impact on your score than payment history.

Sources:

Adam Hayes. FICO Score. Dotdash Meredith. 18 February 2023.

Rajeev Dhir. Creditworthiness: Definition, How to Check and Improve It. Dotdash Meredith. 5 April 2021.

The Investopedia Team. Credit Score: Definition, Factors, and Improving it. Dotdash Meredith. 18 September 2022.

TransUnion. How Credit Scoring Works. TransUnion. 17 November 2020. Retrieved from How Credit Scoring Works | TransUnion.

TransUnion. What is a credit score? TransUnion. Retrieved from What is a Credit Score & How is it Affected | TransUnion.

Create Your Own Website With Webador